Starting May 5th, 2025, federal student loans debt collection is back. If you’re in default, this means the U.S. Department of Education can garnish your wages, seize tax refunds, and report missed payments to credit bureaus again.

Millions of borrowers are affected. If you’re one of them, here’s what you need to know — and what you need to do now to protect your income and credit.

What’s Happening on May 5?

The Department of Education will restart the Treasury Offset Program. This allows the government to collect defaulted federal student loans by taking your tax refund or up to 15% of your disposable wages — without a court order.

You’ll also start seeing missed payments reported to credit bureaus. This already started in January 2025, and it could damage your credit if you don’t act soon.

You Won’t Get Loan Forgiveness — You’ll Get Emails

The Department is not offering mass forgiveness. But it is sending out emails.

If you’re in default, expect to hear from the Federal Student Aid (FSA) office. You’ll be urged to:

- Enroll in an income-driven repayment (IDR) plan

- Make a voluntary monthly payment

- Start loan rehabilitation to eventually remove the default from your credit

The emails will link to myeddebt.ed.gov, where you can take action.

The SAVE Plan Was Blocked — Millions Affected

The Saving on a Valuable Education (SAVE) plan was supposed to help 8 million borrowers make lower, income-based payments.

But in February 2025, a federal court blocked it.

That leaves millions without the plan they signed up for. And without SAVE, more borrowers could fall behind or default, making things worse for those already struggling.

Why This Matters Now

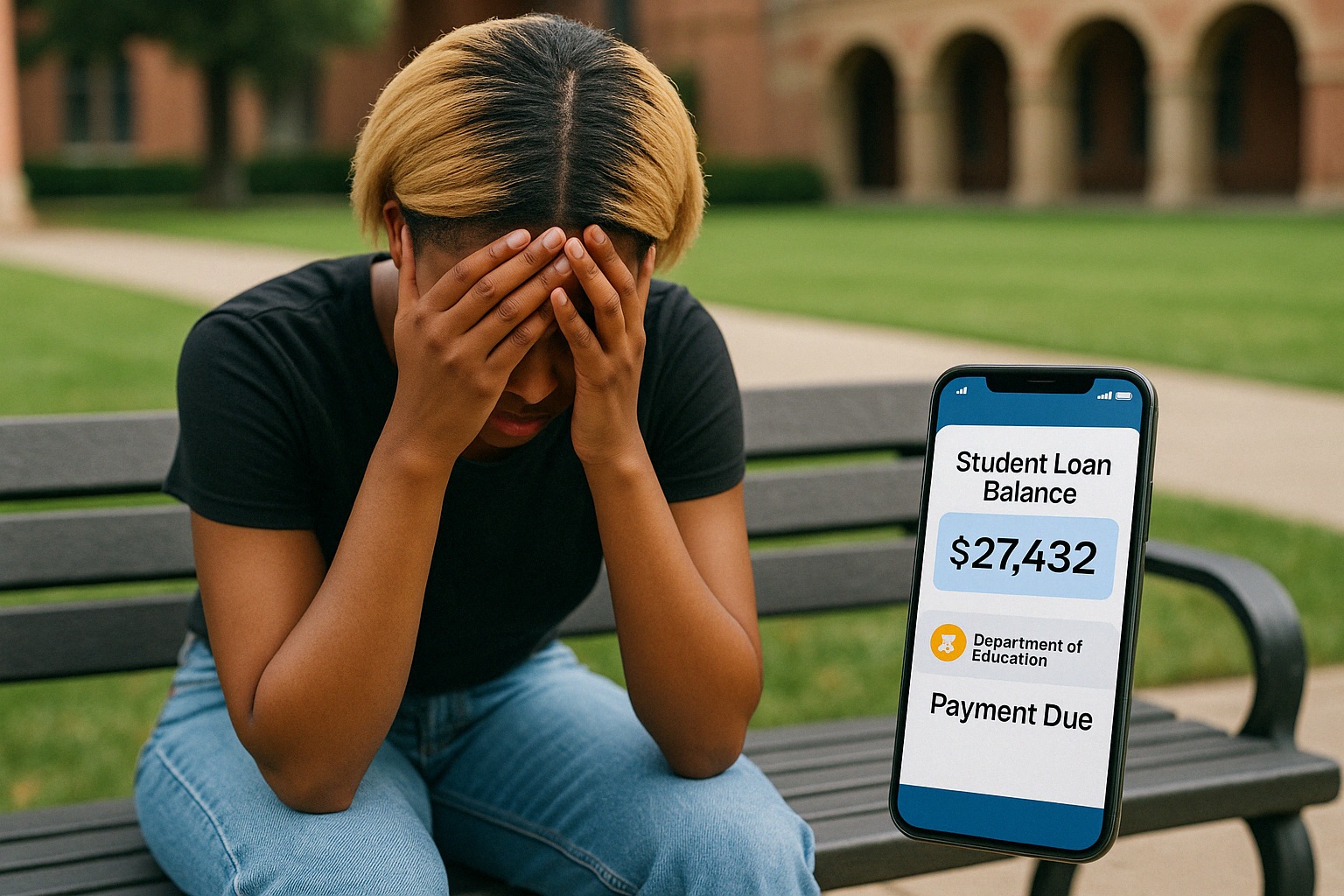

More than 5 million borrowers are already in default. Another 4 million are late on their payments. According to data from the Education Data Initiative, the default rate is over 8%, with nearly half a million new defaults each year.

Once you’re in default for 270 days, the government doesn’t need a court to start collections. They can take your refund, garnish your paycheck, and report you to credit agencies.

And once that process starts, it’s hard to stop without getting out of default completely.

What You Can Do Right Now

If you’re behind on your loans, don’t wait. Here are the most important steps you can take today:

- Check your loan status at StudentAid.gov

- Log in to myeddebt.ed.gov to view your defaulted loans

- Contact the Default Resolution Group to start a repayment or rehabilitation plan

- Enroll in an IDR plan to make affordable monthly payments

- Use tools like the Loan Simulator and the new AI assistant “Aiden” at StudentAid.gov/end-default

The Department is also rolling out a communications campaign with more help — including extended phone hours and simplified IDR enrollment with no annual recertification.

Illegal Collections: Know Your Rights

Not all debt collection is legal.

In January 2025, the Consumer Financial Protection Bureau (CFPB) won a case against the National Collegiate Student Loan Trusts for breaking debt collection laws. They had sued borrowers without proof and tried to collect on debts that were too old.

The Trusts were ordered to pay $2.25 million in relief and stop collecting on some debts.

If you think your lender is doing something wrong, you can file a complaint at the CFPB Complaint Page or email whistleblower@cfpb.gov.

A Quick Look at the Numbers (2025)

| Metric | Value |

|---|---|

| Total Borrowers | 42.7 million |

| Total Federal Debt | $1.6 trillion |

| In Default (360+ days) | 5 million |

| Late-Stage Delinquency | 4 million |

| Average Default Rate | 8.15% |

| Borrowers Affected by SAVE Suspension | 8 million |

The Bottom Line

The pause is over. Student loans debt collection is resuming. And if you’re in default, this could hit your wallet and credit fast.

There’s no bailout coming. No broad forgiveness. But there are steps you can take to avoid wage garnishment, credit damage, and more stress.

Don’t wait for May 5 to take control.

✅ Take Action Now

Visit StudentAid.gov/end-default to explore your options. Share this with someone who’s struggling — it could make all the difference.