Berkshire Hathaway (BRK-B) is having a strange year.

Stocks are down. The S&P 500 is hurting. But Berkshire? It’s up over 16% in 2025.

How is that even possible?

And is it a smart time to buy—or wait?

Let’s break this down.

1. The Stock Is Strong (But Just Dropped)

As of today, April 4, 2025, BRK-B is trading at $530.16. That’s down 1.41% from the previous day. It’s a small dip, sure. But this comes after a strong run.

Over the past year, it’s up 28.36%.

Even in Q1 alone, Berkshire jumped 17.3%, while the S&P 500 fell 4.6%.

So what’s behind this strength?

Two things.

Warren Buffett… and cash.

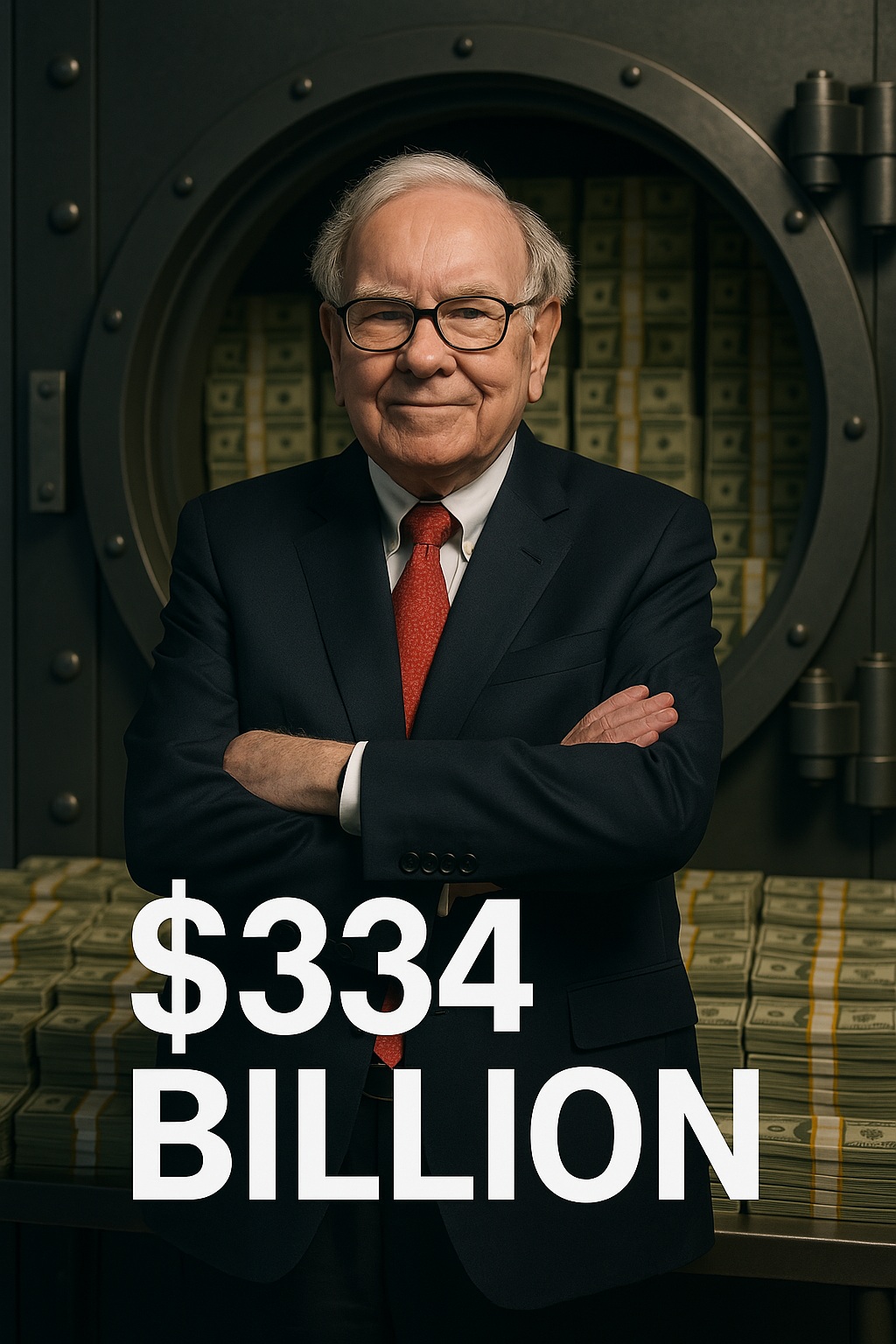

2. Buffett’s Cash Pile Is Getting Massive

Berkshire is sitting on a record $334 billion in cash. Not million. Not even billion with a “small b.” This is Big-B billion. Three hundred thirty-four of them.

Back in early 2022, they had just $106.3B. That’s tripled.

So what does that mean?

It means Buffett’s ready to strike if the market crashes. He has money to buy when others panic. That kind of war chest gives investors confidence. A lot of it.

And maybe that’s why Berkshire keeps rising—even when things look shaky.

3. The Price Might Be Too High Right Now

Here’s the thing. Even with all the good news… the stock might be a bit expensive.

The price-to-book ratio (that’s how much people are paying compared to what the company is worth on paper) is now at 1.8. That’s the highest it’s been in 10 years.

Some investors are nervous about that. They’re waiting. Watching. Hoping for a small dip before buying more.

The price target from analysts? Around $502.00. That’s lower than where it’s trading now.

So yeah, it might be smart to hold off a bit… unless you’re investing long-term.

4. Tariffs Could Hurt Some of Berkshire’s Businesses

President Trump’s new tariffs are no joke. They started in March 2025. Here’s a quick look:

- 25% on goods from Canada and Mexico

- 20% on Chinese goods

- 10% on Canadian energy

So… what does this mean for Berkshire?

Some of their businesses—like railroads (BNSF) and manufacturing (like Precision Castparts)—could see higher costs. Or slower shipments. Or both.

That said, Berkshire’s insurance and utilities? Not really affected.

And overall, the market hasn’t punished the stock. At least, not yet.

5. Earnings Are Coming—and Investors Are Watching

Mark your calendar:

May 4, 2025. That’s the next earnings date.

Last year, operating earnings jumped 27%. Huge. This year, people want to know: What will Buffett do with all that cash?

Will he go shopping?

Will he buy back more stock?

Or just sit on it?

Since 2018, Berkshire has spent $77.8 billion buying back its own shares. That’s helped keep the price strong.

But with valuations this high, some wonder if that’s still the right move.

Quick Recap for Busy Readers

- Price now: $530.16

- Up 16.2% YTD (vs. S&P 500 down 4.6%)

- Record $334B cash

- Price-to-book at 1.8 (10-year high)

- Tariffs may hurt rail & manufacturing

- Next earnings: May 4

- Price target: $502.00

Should You Buy?

If you’re a long-term investor, Berkshire still looks strong.

Great leadership. Tons of cash. Solid businesses.

But… the current price is high.

Maybe too high for some.

If you believe in Buffett and the long game, buying in stages might make sense. If you’re worried about short-term risks or valuation? Waiting could be smarter.

Just don’t ignore this stock.

It’s not every day a company with $334B in cash outperforms the market—during a trade war.